Loan Funding Delayed? Your Financial Impact Explained

You’ve signed the paperwork, passed the credit check, and are counting on that loan to hit your bank account. The expected deposit date comes and goes, and your balance remains unchanged. A delayed loan disbursement is more than a minor inconvenience, it’s a financial event that can trigger a cascade of problems, from missed payments to damaged credit. Understanding the potential consequences and knowing your immediate steps can be the difference between a temporary setback and a long-term financial headache. This guide explores the real-world impact of funding delays, your rights as a borrower, and a clear action plan to navigate the situation.

Protect your finances and get a clear action plan. Visit Resolve Funding Delay to understand your rights and immediate steps.

Immediate Financial Consequences of a Funding Delay

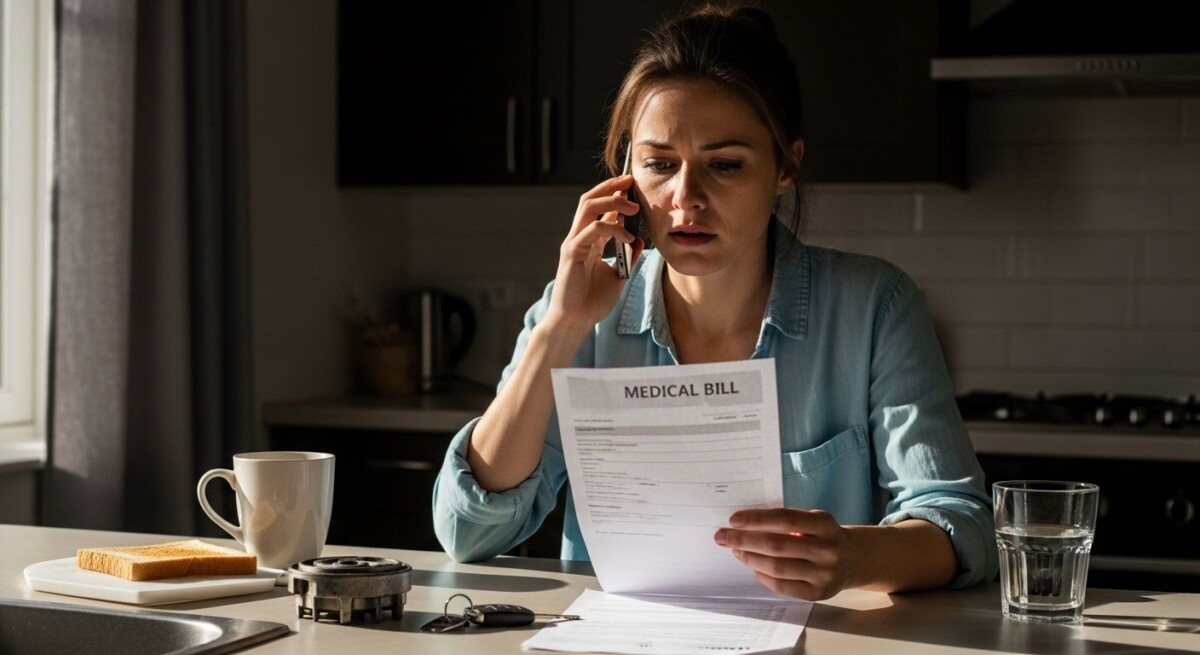

When a loan fails to fund on time, the first and most acute effects are financial. These consequences can materialize quickly, often within days of the missed funding date. If you were relying on those funds to cover specific obligations, the delay creates an immediate shortfall. This can lead to a domino effect where one missed payment causes others. For instance, if you planned to use a personal loan to pay a high-interest credit card bill, the delay means that bill goes unpaid, accruing late fees and additional interest. The stress of managing cash flow without the expected capital can be significant, forcing difficult choices about which bills to prioritize.

Beyond personal bills, a delay can have severe implications for business or time-sensitive transactions. A small business owner awaiting an SBA loan to meet payroll faces not just financial penalties but also a loss of employee trust and morale. An individual using a mortgage bridge loan to close on a new home could lose their earnest money deposit and the property itself if the funding delay causes them to miss the closing date. The immediate fallout is often a combination of tangible costs, like late fees, and intangible costs, like stress and lost opportunities.

Long-Term Credit and Contractual Ramifications

The repercussions of a funding delay extend far beyond the initial week. If the delay causes you to miss payments on other debts, those late payments can be reported to the credit bureaus. Even a single 30-day late payment can significantly lower your credit score, affecting your ability to secure favorable interest rates for years. Furthermore, your new loan agreement itself may have clauses related to funding. While the lender is typically obligated to fund, excessive delays on your part in providing requested documentation could allow them to cancel the agreement altogether.

In some cases, a pattern of funding issues with a particular lender might be a red flag. While legitimate processing delays happen (often due to verification holdups, bank errors, or high application volume), consistent problems could indicate operational issues. It’s crucial to distinguish between a one-time administrative snag and a sign of a problematic lender. A cancelled loan application, especially if it was a hard inquiry on your report, can remain as a note, and while it doesn’t directly hurt your score like a late payment, it doesn’t help your borrowing history.

Your Action Plan: Steps to Take When Funding Is Late

Panic is not a strategy. Taking systematic, documented action is key to resolving the delay and protecting yourself. Your first step should always be to contact the lender directly. Do not rely solely on email, use the phone for a real-time conversation. Have your loan application or reference number ready. Calmly ask for the status of your application and the specific reason for the delay. Is it awaiting final verification? Was there an error in your bank account information? Did the underwriting team request additional documents you haven’t provided? Getting a clear, specific answer is the first step toward a solution.

Once you have identified the cause, you can work to resolve it. Follow up any verbal communication with a summary email to create a paper trail. Document the name of the representative you spoke with, the time and date, and what was promised. Simultaneously, review your own obligations. Did you sign and return all documents promptly? Did you provide accurate bank account details for the direct deposit? Ensuring you have fulfilled your part of the contract strengthens your position when seeking resolution from the lender.

While you work with the lender, you must also engage in financial triage. Contact the creditors you intended to pay with the loan funds. Explain the situation briefly and ask about any possible grace periods or late fee waivers. Many companies have policies for one-time courtesy adjustments, especially if you have a good payment history. Proactive communication here can prevent negative marks on your credit report. To manage this process effectively, follow these steps in order:

Protect your finances and get a clear action plan. Visit Resolve Funding Delay to understand your rights and immediate steps.

- Contact the lender immediately to get a specific reason for the delay.

- Gather and submit any pending documentation requested by the underwriter.

- Verify your banking information with the lender to ensure it is correct.

- Communicate with your creditors to explain the situation and seek short-term relief.

- Document all interactions with the lender, including names, dates, and promises made.

After taking these steps, you may need to evaluate the lender’s response. If the delay is due to their error and is causing you demonstrable harm (like a missed mortgage closing), you may have grounds to formally complain. Start with the lender’s internal customer resolution department. If that fails, you can escalate to relevant regulatory bodies.

When to Escalate and Where to File a Complaint

If the lender is unresponsive, provides contradictory information, or the delay stretches beyond a reasonable timeframe (often more than 5-7 business days past the promised date without a valid, documented reason), it is time to escalate. Your first escalation point is typically the lender’s own customer service supervisor or complaints department. Frame your complaint around the specific harm the delay is causing, referencing your documented communication.

If internal escalation fails, you have several external avenues. For personal loans, including payday or installment loans, you can file a complaint with the Consumer Financial Protection Bureau (CFPB). The CFPB forwards complaints to the company and works to get a response. For state-licensed lenders, your state’s Attorney General office or Department of Financial Institutions is a powerful regulator. For business loans, the Small Business Administration (SBA) Ombudsman may be a resource for SBA-guaranteed loans. Submitting a complaint to these agencies creates an official record and often prompts a faster, more formal response from the lender.

Frequently Asked Questions About Loan Funding Delays

How long is a typical loan funding delay?

A delay of 1-3 business days can occur due to bank processing (ACH transfers). Delays beyond 5-7 business days after an approved and signed offer often indicate an issue requiring your attention, such as additional verification.

Can a lender cancel my loan after approval if funding is delayed?

Yes, in certain circumstances. If the delay is caused by the lender discovering false information, or by your failure to provide required documentation, they may have the right to rescind the approval before funds are disbursed.

Am I responsible for interest during the funding delay?

Typically, the loan interest clock does not start until the funds are actually deposited into your account. Your loan agreement should specify the exact start date of your repayment period, which is almost always tied to the disbursement date.

What is the most common cause of a delayed loan?

The most frequent causes are verification holdups (income, employment, identity), errors in the bank account information provided by the borrower, and high application volume slowing the lender’s internal processing.

Should I apply for another loan if the first one is delayed?

This is generally not advisable. A second application will trigger another hard credit inquiry, further lowering your score. It also risks being approved for two loans simultaneously, which you may not be able to afford. Focus on resolving the delay with the first lender.

A delayed loan is a test of both financial preparedness and procedural diligence. By understanding the potential impacts, from immediate cash shortfalls to long-term credit damage, you can respond strategically rather than reactively. The core of managing this situation lies in proactive communication, meticulous documentation, and knowing your recourse options. While frustrating, a funding delay handled correctly can be a navigable obstacle, not a financial disaster. Protect your interests, fulfill your obligations, and use the tools available to ensure the process concludes in your favor.

Protect your finances and get a clear action plan. Visit Resolve Funding Delay to understand your rights and immediate steps.

About Ethan Harper

Related Posts